Let’s say your AC quits in July. You call a technician. He pokes around for twenty minutes and hands you a quote for $4,800. You feel a little sick. You remember seeing ads for home warranties and think Should I have done that?

Good news: you’re asking the right question. Bad news: the answer isn’t simple.

A home warranty can save you money on repairs. But it can also cost you more than you’d spend just paying out of pocket, depending on your home, your appliances, and what the contract actually says. So before you pull out your credit card, here’s everything you need to know.

First — What Is a Home Warranty, Anyway?

A home warranty is basically a service contract. You pay a monthly or yearly fee, and when a covered appliance or home system breaks down, the warranty company sends someone to fix it. You just pay a smaller fee for the service call.

It’s not the same as homeowners’ insurance. Your insurance covers damage from things like fires, floods, or break-ins. A home warranty covers things that just… wear out. The fridge stops cooling. The furnace stops heating. The garbage disposal decides it’s done.

When that happens, you file a claim, pay your service call fee (usually $75–$150), and a contractor comes out. If the repair or replacement is covered, the warranty picks up the rest of the cost. Simple enough in theory.

In practice, there’s more to it. But we’ll get there.

What Does a Home Warranty Usually Cover?

Coverage varies by plan, but most standard home warranty plans include:

| What’s Covered | Typical Plan | Premium Add-On |

|---|---|---|

| Heating system (furnace) | ✅ Yes | — |

| Air conditioning | ✅ Yes | — |

| Plumbing system | ✅ Yes | — |

| Electrical system | ✅ Yes | — |

| Water heater | ✅ Yes | — |

| Refrigerator | ✅ Yes | — |

| Oven / range | ✅ Yes | — |

| Dishwasher | ✅ Yes | — |

| Washer & dryer | ✅ Yes | — |

| Pool or spa | ❌ No | ✅ Add-on |

| Roof leak | ❌ No | ✅ Add-on |

| Second refrigerator | ❌ No | ✅ Add-on |

| Septic system | ❌ No | ✅ Add-on |

Notice what’s not on the standard list: structural problems, cosmetic damage, pre-existing issues, code violations, or parts that aren’t mechanical. That last one trips people up a lot. Your warranty might cover your refrigerator but exclude the ice maker, water dispenser, and drawer rails. Yep — it happens.

The Real Numbers: What Does a Home Warranty Cost in 2026?

Here’s where the “does it save money” question actually starts to take shape.

What you pay for the warranty:

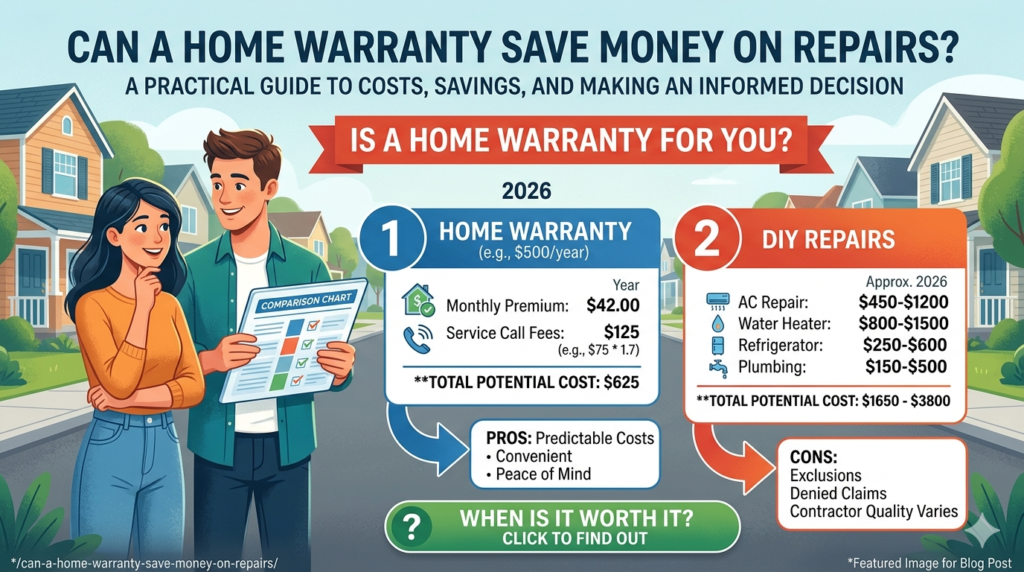

- Average monthly premium: $73/month (about $876/year)

- Service fee per call: $75 to $150 (most commonly $100–$125)

- A year with two service calls: roughly $1,076 to $1,176 total out of pocket

What repairs cost without a warranty:

| Repair or Replacement | Typical Cost (No Warranty) |

|---|---|

| HVAC system replacement | $5,000 – $10,000 |

| Water heater replacement | $1,000 – $3,000 |

| Major plumbing repair | $500 – $4,000 |

| Electrical panel repair | $500 – $2,500 |

| Refrigerator repair | $200 – $330 |

| Refrigerator replacement | $430 – $10,600 |

| Oven / range repair | $100 – $430 |

| Dishwasher repair | $160 – $300 |

| Washer or dryer repair | $150 – $400 |

The contrast is pretty clear. One HVAC replacement could cost you more than five years of warranty premiums. A single water heater swap could pay for two or three years of coverage.

But here’s the catch: that math only works if your claim gets approved. And not every claim does. We’ll cover why in a minute.

Can a Home Warranty Actually Save You Money? (Real Example)

Here’s a scenario that plays out pretty often.

Marcus bought a 12-year-old house in 2024. He signed up for a home warranty at $65/month — about $780/year — with a $100 service call fee.

In year one, his water heater gave out. Replacement cost: $1,400. He paid the $100 service fee. The warranty covered the rest. Net savings that year: $1,200 after you subtract his annual premium.

In year two, nothing broke. He spent $780 and got nothing back. He started second-guessing himself.

In year three, his HVAC compressor failed. Repair cost: $2,200. He paid $100. The warranty handled it. Over three years, Marcus paid about $2,440 total (premiums + two service fees) and avoided $3,600 in repair bills. He came out ahead by over $1,100.

That’s what a home warranty can do. It doesn’t always work this cleanly — but for homes with aging systems, it often does.

Home Warranty: Pros and Cons

Let’s keep this straightforward.

✅ Pros

Predictable monthly cost. Instead of a random $3,000 surprise, you’re paying $65/month. That’s easier to budget around.

No contractor hunting. The warranty company sends someone to you. You don’t have to scroll Yelp at midnight hoping someone’s available.

One call handles it. File the claim, pay the fee, done. For people who hate dealing with repairs, that’s a real quality-of-life win.

Can cover multiple things in one year. If your oven breaks in March and your dishwasher breaks in August, you’ve only paid two service fees — not two full repair bills.

Good protection for older homes. The older your systems, the higher the odds that something breaks. A warranty is essentially a bet that at least one thing will need fixing. With older appliances, that’s usually a safe bet.

❌ Cons

Claims can get denied. This is the big one. Pre-existing issues, missed maintenance, unapproved repairs — any of these can get your claim rejected. You paid the premiums and still get a repair bill.

You don’t pick the contractor. The warranty company uses its own network. Some of those contractors are great. Some aren’t. You’re stuck with whoever shows up.

Coverage limits cap what they’ll pay. Many plans cap HVAC coverage at $1,500 per contract year. If your unit needs a $7,000 replacement, you’re paying the difference.

Newer homes don’t need it. If your appliances all come with manufacturer warranties, you’re essentially paying twice for coverage you already have.

Fine print is thick. Seriously. There are exclusions buried in there that most people don’t read until they’re trying to file a claim.

When a Home Warranty Is Worth It

A home warranty tends to make real financial sense when:

- Your major systems and appliances are 8 to 15 years old. That’s the sweet spot where things start failing, but parts are still available.

- You don’t have a dedicated repair fund. Most financial advisors suggest setting aside 1–3% of your home’s value each year for repairs. A $400,000 home means $4,000–$12,000 annually. If that’s not realistic right now, a warranty fills the gap.

- You just bought an older home, and you’re not sure what you inherited. Even a good home inspector can miss things. A warranty buys you a cushion while you get familiar with the house.

- You’re a landlord. Tenant repairs are unpredictable and time-sensitive. A warranty makes costs manageable and removes the headache of sourcing contractors.

- You want convenience alongside savings. Some people genuinely value not having to manage repair logistics. That’s a real benefit, even if it’s hard to put a dollar figure on it.

When a Home Warranty Probably Isn’t Worth It

Skip the warranty if:

- Your appliances are brand new. Manufacturer warranties already cover them. You don’t need to pay double.

- You have a solid repair savings account. If you can cover a $5,000 HVAC repair without blinking, you’re better off keeping your premium payments. If nothing breaks, you keep that money.

- Your home is very old with hard-to-find parts. Warranty companies may offer a cash payout based on depreciated value, which usually doesn’t cover actual replacement costs.

- You want to choose your own contractors. If you have a trusted plumber or HVAC tech you’ve worked with for years, a warranty forces you to use someone else.

Why Do Home Warranty Claims Get Denied?

This is probably the most important section in this whole post. Because the number one complaint about home warranties is that claims get denied — and it almost always comes back to one of these reasons:

Pre-existing conditions. If the problem existed before your coverage started, it’s not covered. A warranty technician is trained to spot signs of pre-existing failure. If they see rust, age-related deterioration, or damage that clearly wasn’t new, the claim may be rejected.

Skipped maintenance. Warranties generally cover normal wear and tear — not neglect. If your HVAC system breaks down and there’s no record of regular filter changes or servicing, the company may argue that poor maintenance caused the failure.

DIY fixes. If you tried to repair something yourself before filing a claim, you could void the coverage. Always call the warranty company first, before touching anything.

Excluded parts. Your refrigerator is covered — but the specific part that broke might not be. Ice makers, dispensers, drawer tracks, door gaskets — these often get carved out in the fine print.

Using your own contractor. If you called an outside repair person and paid them before going through your warranty, don’t expect reimbursement. The company needs to be involved in the process from the start.

How to Make the Most of a Home Warranty

If you decide a warranty is the right move, here’s how to get actual value from it:

Get quotes from at least three companies. Monthly premiums range from $30 to $90 for similar coverage. The spread is wide. Shopping around saves money before you even use the warranty.

Pick your service fee based on how often you’ll use it. A lower service fee means higher monthly premiums — and vice versa. If you have an older home with multiple ageing systems, a lower service fee is usually the smarter trade.

Read the contract before signing. Yes, the whole thing. Look specifically at exclusion lists, coverage caps per item, and what counts as a “pre-existing condition.” You need to know this before you need to file a claim, not during.

Keep your maintenance records. Change your HVAC filters. Get your systems serviced. Keep receipts. If a claim ever gets contested, proof of maintenance is your best defence.

Look up contractor reviews for your area. Some warranty companies have strong contractor networks in certain regions and weaker ones elsewhere. Reviews on sites like ConsumerAffairs and the Better Business Bureau can tell you a lot before you commit.

Home Warranty vs. Just Saving the Money — Side by Side

| Home Warranty | Self-Insuring (Savings Account) | |

|---|---|---|

| Monthly cost | $35–$90/month | Whatever you set aside |

| Big repair coverage | Yes (within limits) | Yes (if you’ve saved enough) |

| Coverage limits | Capped per item/year | No cap — it’s your money |

| Claim denials | Possible | Never — you control it |

| Contractor choice | Assigned by company | Your choice |

| Best for | Older homes, tight budgets | Newer homes, strong savings |

| Unused premium | Gone | You keep it |

Neither option is automatically better. It comes down to your specific situation: the age of your home, your financial cushion, and how much you value the convenience factor.

The Bottom Line

Can a home warranty save money on repairs? Yes, genuinely yes if your appliances and systems are getting up there in age, if you’d struggle to cover a surprise $4,000 repair, and if the claim actually goes through.

It’s not magic. It’s a contract with rules. And the people who get burned by home warranties are almost always the ones who signed up without reading those rules first.

Here’s a simple decision guide: If your HVAC, water heater, or major appliances are between 8 and 15 years old and you don’t have a dedicated repair fund, a home warranty is probably worth it. If everything’s newer or you’ve got savings built up, skip it and put that $73/month somewhere useful.

The warranty is only as good as what it actually covers. So read the contract, know the exclusions, and go in with clear eyes.

Ready to compare home warranty plans? Look at what’s covered, what the limits are, and get at least two or three quotes before you commit.