Here’s a scenario that plays out more often than people realize.

A guy rear-ends someone at a stoplight. Nothing dramatic — the other driver walks away. But a few months later, there’s a lawsuit. Medical bills. Lost wages claims. The total? Just over $80,000. His state-minimum auto policy covered $25,000. The rest came out of his savings.

He wasn’t reckless. He just had no idea his coverage was that thin.

That’s the problem most people have with insurance. They sign up, pay the premium, and assume they’re covered. They’re not asking how much insurance coverage you really need — they’re just hoping the number they picked is close enough.

It usually isn’t.

This post is going to change that. We’re breaking down the four types of insurance that matter most — auto, life, home, and health — and giving you real numbers, not vague ranges.

Why the Minimum Is Almost Always the Wrong Answer

State minimums exist so people can legally drive or own a home. They weren’t designed to actually protect you.

Auto liability minimums in many states are set at levels that haven’t moved in decades. Medical costs have. Repair bills have. Lawsuit settlements have. A single ER visit after a crash can cost $20,000 or more before the hospital even gets to the serious stuff.

Most state minimums cover a fraction of that.

The same thing happens with homeowner’s liability, employer life insurance plans, and the cheapest health plan your HR department offers. They’re starting points, not finish lines.

So the real question when you’re figuring out how much insurance coverage you really need isn’t “what’s the minimum?” It’s “what would I actually lose if something went wrong tomorrow?”

That answer is almost always more than whatever you’re currently carrying.

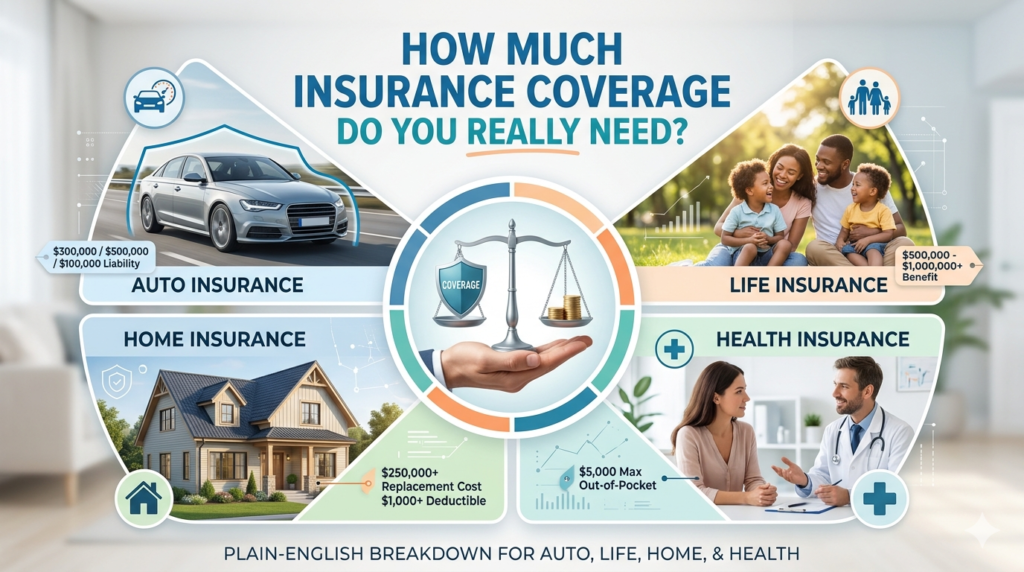

Auto Insurance: What You Actually Need Behind the Wheel

Liability Coverage — Get This Right First

Liability is the part of your auto policy that pays for damage and injuries you cause to other people. It’s shown as three numbers. Something like 100/300/100 means:

- $100,000 per injured person

- $300,000 total per accident

- $100,000 for property damage

Most insurance professionals will tell you that 100/300/100 is the real floor — not a premium option. And honestly, that’s a fair call. The average bodily injury claim runs over $26,000. A serious multi-person accident can blow past six figures fast.

Here’s a straightforward way to think about your limits:

| Your Assets | Coverage to Carry |

|---|---|

| Under $50,000 | 50/100/50 |

| $50,000 – $300,000 | 100/300/100 |

| Over $300,000 | 250/500/250 + umbrella policy |

The reason your assets matter: if a court awards more than your policy covers, they can come after what you own. Your savings. Your home equity. Your retirement account. Your coverage should be a wall between your wallet and that outcome.

Collision and Comprehensive — Know When to Keep Them

If you’re still making payments on your car, your lender decides this for you. They’ll require both.

If you own your car outright, here’s a simple gut-check: if your annual premium for collision and comprehensive is close to 10% of what your car is worth, it’s probably time to drop them. An older car worth $4,000 isn’t worth paying $400 a year to protect.

Uninsured Motorist Coverage — Don’t Skip This One

Roughly 1 in 8 drivers on the road is uninsured. If one of them hits you, your regular liability policy doesn’t help you — it only covers what you owe others. Uninsured motorist coverage fills that gap. Match it to your liability limits and move on.

Gap Insurance — Worth It on a New Car

New cars lose value fast. In the first couple of years, you can easily owe more on the loan than the car is worth. If it’s totaled, your insurer pays market value — not what you owe. Gap insurance covers that difference. It’s inexpensive, and on a new vehicle, it’s a smart call.

Life Insurance: How Much Is Actually Enough?

Most employer life insurance plans give you one to two times your salary. If you earn $60,000, that’s a $60,000–$120,000 payout. Sounds decent until you think about a mortgage, a couple of kids, and ten-plus years of living expenses. Suddenly, it’s not even close.

Knowing how much insurance coverage you really need for life starts with a realistic look at what your family would actually need to keep going without your income.

The 10x Rule — A Quick Starting Point

Multiply your annual income by 10. If you make $70,000, aim for at least $700,000 in coverage. It’s simple and gives you a usable baseline. But it doesn’t account for debt or kids’ education, so treat it as a floor, not a final answer.

The DIME Formula — More Accurate

This one’s worth the extra five minutes:

- D — Debt: Everything you owe. Car loans, credit cards, student loans.

- I — Income: Your annual salary × the number of years your family would need support (usually 10–15).

- M — Mortgage: What’s left on your home loan?

- E — Education: Estimated cost to put your kids through school.

Add those four numbers together. That’s a much more honest picture of your coverage needs.

Quick example: $70,000 income × 12 years = $840,000. Add a $240,000 mortgage, $25,000 in debt, and $60,000 for education. Total: $1,165,000. That’s a lot more than most employer plans offer — and that’s kind of the point.

Term vs. Whole Life

For most people, term life is the smarter move. You pick a term — usually 15 to 30 years — and pay a lower premium for high coverage during the years it matters most. Raising kids. Paying off a mortgage. Building savings.

Whole life covers you permanently and builds cash value, but the premiums are significantly higher. It makes sense for specific estate planning situations. For the average family just trying to protect their income? Term wins.

Homeowners Insurance: Don’t Make This Common Mistake

The biggest mistake homeowners make is insuring their house for its market value instead of what it would actually cost to rebuild it.

Those two numbers are often very different. And when disaster strikes — a fire, a tornado, a total loss — the gap between them becomes your problem.

A 2025 study found that nearly three-quarters of Colorado homeowners had underinsured homes. That’s not a Colorado problem. That’s a nationwide pattern. Construction costs have climbed sharply in recent years, and plenty of older policies haven’t kept up.

The 80% Rule and Why It Matters

Most insurers require your dwelling coverage to be at least 80% of your home’s full replacement cost. Drop below that, and you can face a penalty — the insurer pays a reduced amount even on partial claims.

The smart move: insure for 100% of rebuild cost. Get a replacement cost estimate, not a market appraisal. They’re not the same thing.

What Each Part of Your Policy Should Cover

| Coverage | What It’s For | Suggested Amount |

|---|---|---|

| Dwelling | Your home’s structure | 100% of rebuild cost |

| Other Structures | Detached garage, fence, shed | ~10% of dwelling limit |

| Personal Property | Your stuff inside | 50–70% of dwelling limit |

| Liability | Injuries on your property | $300,000–$500,000 |

| Loss of Use | Temporary housing costs | 20–30% of dwelling limit |

Liability — Most People Carry Too Little

Standard policies often default to $100,000 in personal liability. That sounds like a lot until someone slips on your steps and hires a lawyer. Legal defense costs add up even when you’re not at fault.

Most financial advisors recommend bumping liability to at least $300,000–$500,000. If your total assets are higher than that, consider an umbrella policy on top.

What Your Policy Won’t Cover

Flood damage and earthquake damage aren’t included in a standard homeowners policy. If you’re in a flood-prone or seismically active area, you need a separate policy for those — and it’s not optional, it’s essential. Jewelry, art, and high-value items often need their own scheduled endorsements, too.

Health Insurance: Match the Plan to Your Life

Health insurance works differently from the others. You’re not choosing a dollar limit — you’re choosing a structure. And the right structure depends almost entirely on how often you actually use healthcare.

If you have ongoing health needs — prescriptions, specialist visits, planned procedures — a lower deductible plan with higher premiums usually saves money overall.

If you’re generally healthy and rarely see a doctor, a high-deductible health plan (HDHP) paired with a Health Savings Account (HSA) often makes more sense. You pay less in premiums, and your HSA contributions go in tax-free.

The honest test: add up what you’d pay in annual premiums plus likely out-of-pocket costs for each plan option. The cheaper-looking premium isn’t always the cheaper plan.

Umbrella Insurance: The Coverage Most People Don’t Know They Need

If your net worth is growing, home equity, retirement savings, investments, and an umbrella policy are some of the smartest things you can add.

It sits on top of your auto and homeowners policies. When a claim exhausts those limits, the umbrella kicks in. A $1 million umbrella policy typically runs $150–$300 per year. That’s not a lot of money for a lot of protection.

It’s particularly worth thinking about if you have a pool, a trampoline, a dog, or a teenage driver. Those are all liability magnets, and standard policies weren’t built for worst-case versions of them.

The Short Version: Real Coverage Benchmarks

| Insurance Type | What Most People Have | What Actually Protects You |

|---|---|---|

| Auto Liability | State minimum (often 25/50/25) | 100/300/100 minimum |

| Life Insurance | 1–2x salary | 10–15x salary (DIME formula) |

| Home Dwelling | Market value | 100% of rebuild cost |

| Home Liability | $100,000 | $300,000–$500,000 |

| Health | Cheapest available plan | Matched to your actual usage |

One Last Thing

Insurance is easy to ignore when nothing bad is happening. That’s exactly when it’s worth reviewing.

Check your policies once a year. After you get married, have a kid, buy a home, or get a raise, check again. Life changes faster than most policies do, and the gap between what you have and what you actually need tends to grow quietly.

If your situation is complicated, sit down with an independent insurance broker. Not a captive agent who works for one company, but an independent one who can shop multiple carriers and tell you what you’re actually missing.

Figuring out how much insurance coverage you really need isn’t a one-time thing. It’s something worth revisiting. The good news? Once you know what you’re looking for, it doesn’t take long.

Disclaimer

This article is for general informational purposes only and does not constitute professional insurance or financial advice. Coverage needs vary based on individual circumstances, state laws, and provider terms. Always consult a licensed insurance professional for guidance specific to your situation.